In the modern investing landscape, few narratives have captured the public’s attention as powerfully as the rise of the “Magnificent Seven” – Apple, Microsoft, Alphabet, Amazon, Meta, Tesla, and Nvidia. These tech giants now represent roughly a third of the S&P 500, shouldering a significant share of the index’s recent gains.2 But as we look to the future, a pressing question emerges: should investors place so much faith – and capital – in such a concentrated slice of the market?

For investors using strategies like those of Inspire ETFs, which intentionally avoid companies that fail to align with biblical values, the absence of the Mag 7 might seem like a significant disadvantage. After all, these seven giants have been among the market's primary growth drivers in recent years. Yet, history and recent market data suggest a different perspective – one where diversified, values-based investing can still yield competitive returns.1,3,4

Market history is full of cautionary tales about the risks of over-concentration. In the 1960s and early 1970s, the “Nifty Fifty” – a group of blue-chip stocks like Polaroid, Xerox, and Eastman Kodak – were once considered “must-own” investments. They were seen as industry-defining companies with seemingly unassailable business models.

However, many of these former giants were eventually toppled by technological disruption, mismanagement, or changing consumer tastes. Xerox, once synonymous with office innovation, struggled through decades of restructuring. Polaroid went bankrupt – twice. Kodak, despite pioneering digital photography, failed to adapt to the digital era and paid a heavy price.

The lesson here is clear: even the most dominant companies can lose their edge. Figure 1 illustrates this point by tracking the turnover among the top 10 largest companies in the S&P 500 since 1985, highlighting the transient nature of market leadership.2

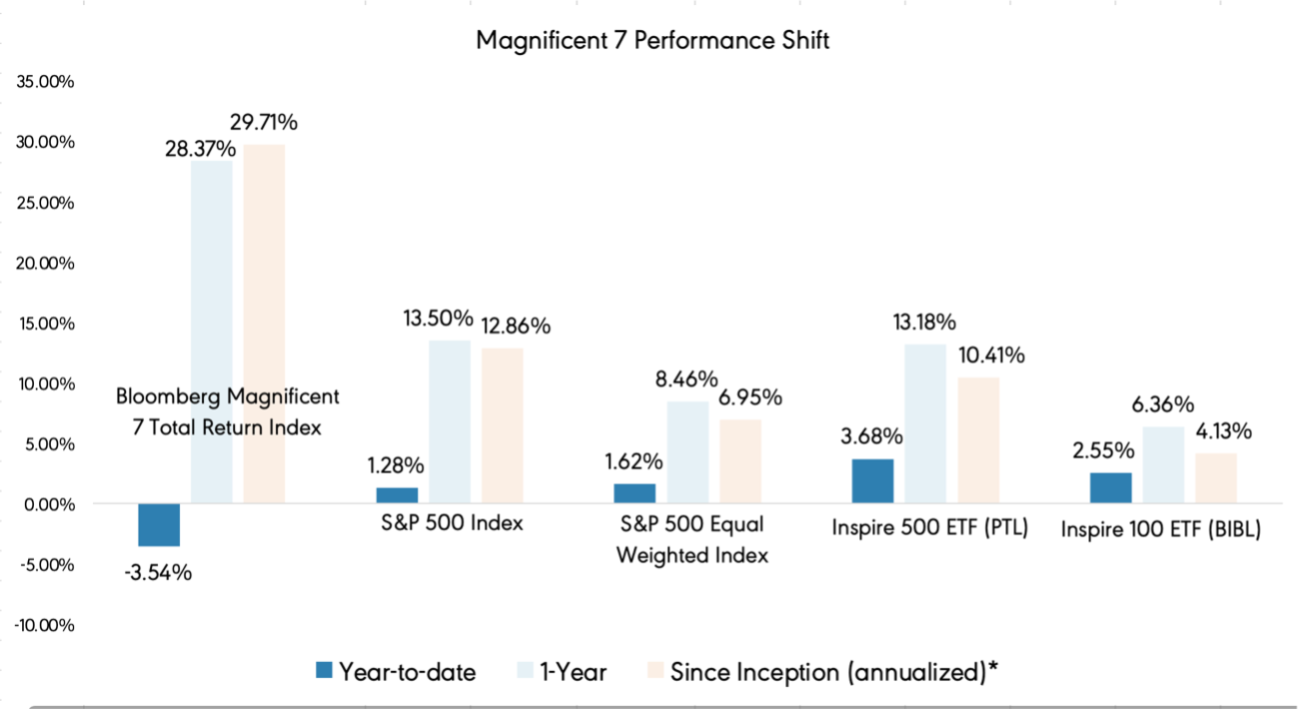

This year’s market performance serves as a timely reminder of the potential pitfalls of over-relying on the Mag 7. Despite their dominant market positions, several of these tech giants have fallen short of expectations, facing headwinds like regulatory scrutiny, stretched valuations, and slowing growth. As a result, the market-cap-weighted S&P 500 has underperformed more diversified benchmarks, including the Equal-Weighted S&P 500 and Inspire’s own large-cap ETFs – Inspire 500 ETF (PTL) and Inspire 100 ETF (BIBL) – both of which are currently outpacing the S&P 500.1,3

This divergence serves as a reminder that diversification matters. When a handful of companies account for approximately a third of an index’s weight, investors face an outsized risk from any single downturn or disruption.

While the Mag 7 may continue to play a significant role in the market, history suggests that no group of companies maintains dominance indefinitely. Excluding these companies due to a values-based investing approach doesn’t doom investors to underperformance. Instead, it may offer long-term advantages when market conditions shift, rewarding those who choose a broader, more diversified path.

Important Risk Information

Investors cannot invest directly in an index and unmanaged index returns do not reflect any fees, expenses or sales charges.

Inspire, the adviser, provides the index for the Inspire Funds to track. The indexes use software that analyzes publicly available data relating to the primary business activities, products and services, philanthropy, legal activities, policies and practices when assigning Inspire Impact Scores to a company. As the Fund may not fully replicate the Index, it is subject to the risk that investment management strategy may not produce the intended results. Past performance is no guarantee of future results.

There is no guarantee that the Funds will achieve their objective, generate positive returns, or avoid losses. Before investing, carefully consider the funds’ investment objectives, risks, charges and expenses. To obtain a prospectus which contains this and other information, call 877.658.9473, or visit www.inspireetf.com. Read it carefully. The Inspire ETFs are distributed by Foreside Financial Services LLC., Member FINRA. Inspire and Foreside Financial Services LLC are not affiliated. Copyright © 2026 Inspire. All rights reserved.